The Slivova gold deposit is an intrusive related, stratiform massive to disseminated gold-bearing and

base metal mineralogy hosted in Cretaceous aged calcareous sediments.

Multisource Error: Missing image size attribute for: image attribute. Please add it to attributes list. Special Attribute -> Image Size

License

Exploration

Location

Kosovo

Area

30.5 km2

Ownership

Western Tethyan is Earn-in to 85% of the project. Predetermined Earn-in and development milestones

Recent work

Surface geochemistry, MRE, PEA, EIA ongoing

Nearterm

Trenching, exploration and Infill drilling program, EIA, SIA

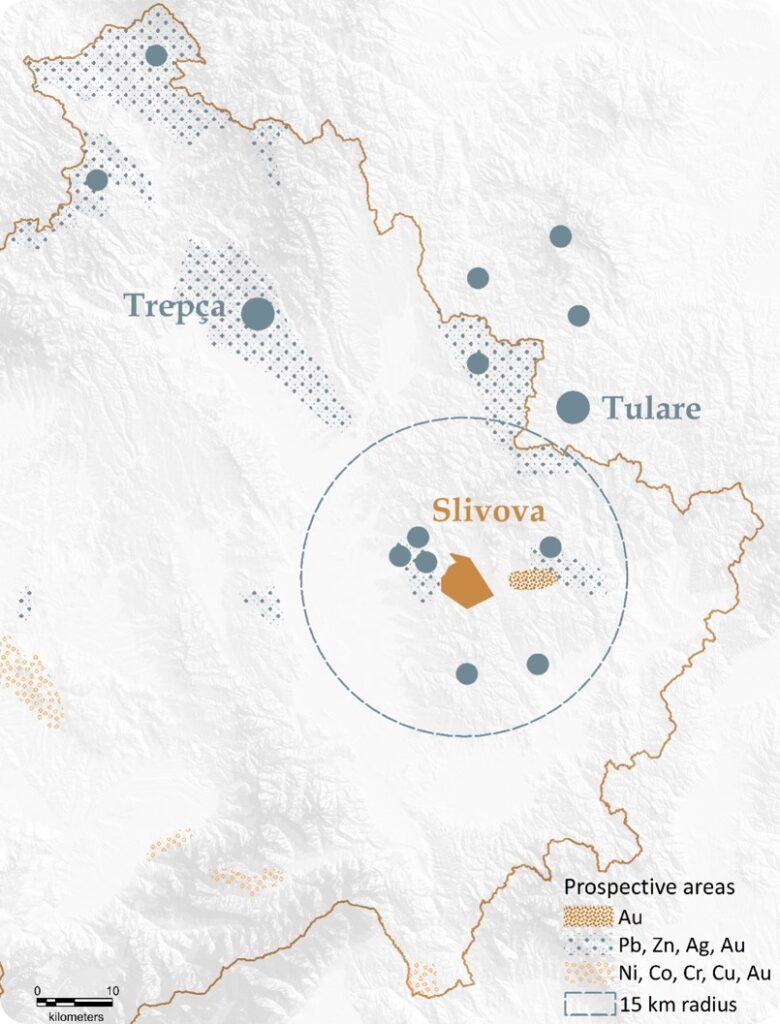

Proximity

To two historical mines and four undeveloped deposits in 15km radius

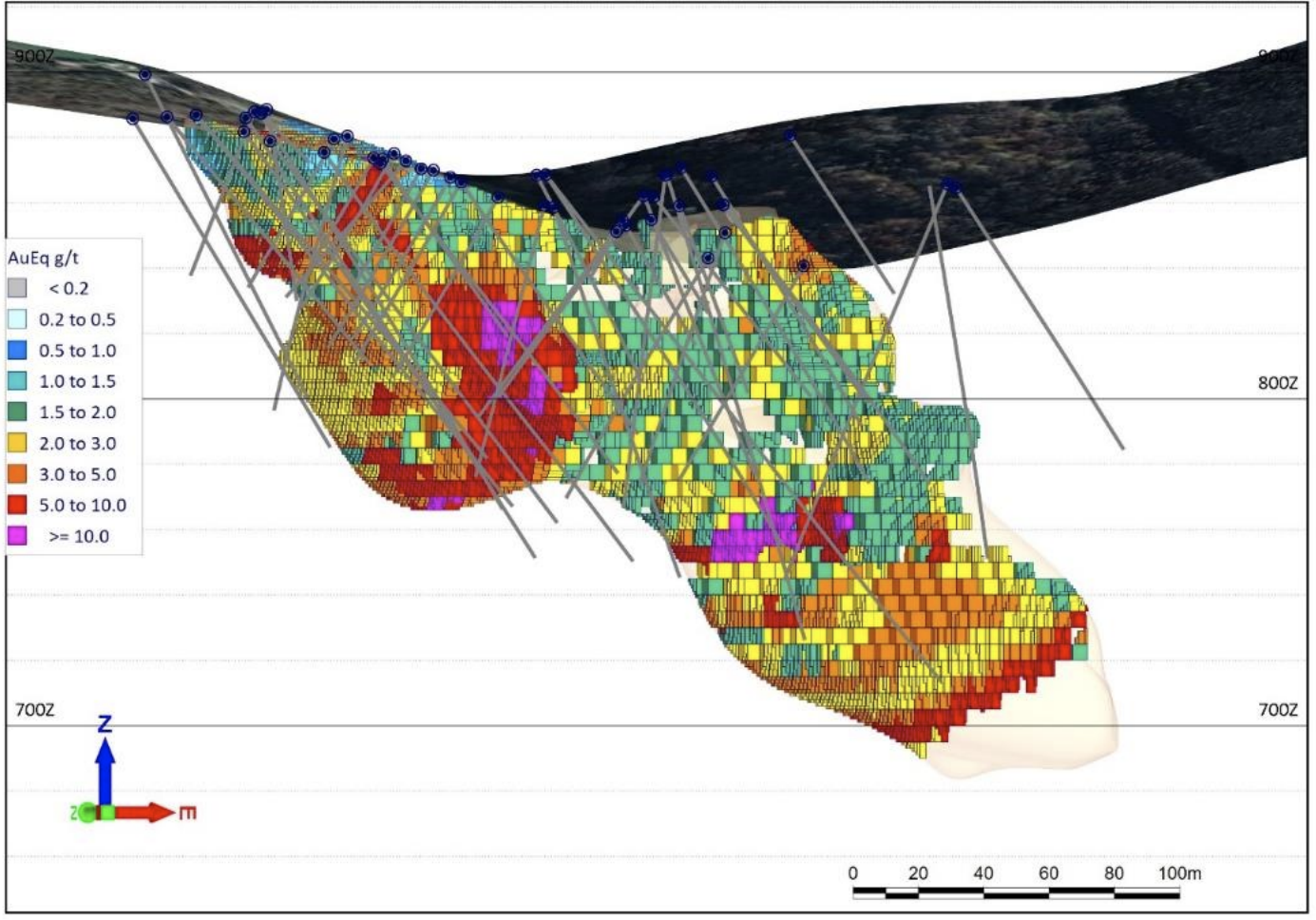

Estimated Mineral Resources for Slivova. Numbers are rounded to an appropriate number of significant figures and as such discrepancies may exist between individual values, products and totals.

The independent Qualified Person responsible for Mineral Resource disclosure, as defined by NI 43-101, is Mr. Richard Siddle, MSc, MAIG, of Addison Mining Services Ltd. The effective date of the Mineral Resource Estimate is 22 June 2023.

Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. There is no certainty that all or any part of the Mineral Resource will be converted to Mineral Reserves.

A gold equivalent (AuEq) grade was calculated for each block using the formula AuEq = (Ag g/t x 0.05) + Au g/t. It is the opinion of the Qualified Person that all elements included in the Au Equivalent calculation have a reasonable prospect of being recovered and sold, the calculation of the Au equivalent value considers the relative recovery and payability of each element (recovery by cyanide leaching of 93.4% for gold and 50% for silver and 95% and 85% payability, respectively, as informed by metallurgical test work completed to date) as well as the assumed commodity prices

Reasonable prospects of eventual economic extraction are satisfied by the estimation of break-even cut-off grades for each anticipated mining scenario (0.5g/t AuEq for open pit and 1.5g/t AuEq for underground mining). These cut-off grades were used to report the Mineral Resource. The cut-off grades were estimated on the basis of the following assumptions: a gold price of US$1850/oz (selected following consideration of (1, 2 and 3 year trailing average LMBA gold price and LMBA 2023 average forecast gold price, a silver price of US$20/oz, underground mining costs of US$43.7/t, processing costs (including tailings disposal) of US$29.5/t and G&A costs of US$3/ROMt.

Estimates in the above table have been rounded to three significant figures for Measured and Indicated Resources and two significant figures for Inferred Mineral Resources

CIM Definition Standards for Mineral Resources have been followed.

The independent Qualified Person for Resources is not aware of any additional known environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues that could materially affect the Mineral Resource Estimate.

The Mineral Resource figures set out above are quoted gross with respect to the Project. WTR of which Ariana owns 75%, has yet to establish a net attributable interest under the Earn-in and accordingly, no separate net attributable figures are reported.

Western Tethyan Resources is the operator of Slivova.

Estimated Mineral Resources for Slivova. Numbers are rounded to an appropriate number of significant figures and as such discrepancies may exist between individual values, products and totals.

Total Mineral Resources (Gross to the Project)

Open Pit Resources Above 0.5g/t AuEq

Underground Resources Above 1.5g/t AuEq

Mineral Resource Estimate

Mine Design

A revised approach to the mining of Slivova involves a small starter pit to access the outcropping mineralised gossan area, followed by underground extraction of the gold resource below the open pit at an appropriate extraction rate to suit the size and grade of the deposit. Mine design involved a more detailed analysis of the potential mining method and a mineable stope optimisation exercise to fully assess and define the underground stoping extents. A geotechnical review was undertaken to validate extraction methods. Ore zones and host rocks are either non-calcareous or calcareous sequences of altered sedimentary rocks with ore zone strengths varying between 45 MPa and 50 Mpa. Mine design was adapted to be flexible to varying competencies of host rock, particularly in the contact areas. The starter pit is designed to be mined from the top bench downwards with ore being accessible and extracted immediately, i.e., there is no requirement or need for any pre-stripping. It has been assumed that this small open pit can be mined by local contractors who have quarries within the vicinity of the proposed mine at Slivova. The revised starter pit design is also situated such that there is now no requirement for stream re-alignment where the pit can be accessed for initial extraction via existing tracks on the north side of the stream. Pit extents minimise the impact on the surrounding countryside and local communities. Due to the requirement for a 25 m crown pillar the bottom bench was modified to a base of 865 mRL. Bench access was linked into the existing tracks and roads on the site. This allows for easy access to each bench for overburden and ore removal without the need for any ramps. Access to the bottom bench is directly in from topography. Pit operations cease after Year 1. Underground access is envisaged as a portal developed directly into the south valley wall, supporting mining typically by sublevel open stoping, unless ore zone geometry dictates a step down to cut-and-fill methods. Main sublevels are 20 m, with stoping separated 25 m from the open pit bottom by a crown pillar which will be mined by sublevel caving methods at the end of mine life. Mining is suggested to be via small teams of approximately 16 people per shift, using small diesel fleet appropriate for production at between 300 t/day and 400 t/day. Mined material to be trammed directly from underground operations through the portal to the primary crusher tip located at the plant site on the saddle of the southern ridge 500 m to the east.

Recovery Methods

Results of extensive characterisation and testing of the Slivova ore by a range of methods suggest that treatment would be via carbon-in-leach (“CIL”) methods, delivering gold recovery of 92-94.5% and silver recovery of 19.8-22.5%. Some gold may be extracted via gravity recovery methods. Nominal plant throughput will be 142,000 tpa, with primary, secondary and tertiary crushing of the ore, followed by ball milling to 106 mm and leaching of the ore by CIL methods. Loaded carbon is stripped, with electrowinning and final EAF smelting of the doré to bullion on site.

Environmental

The environmental and social work completed to date is in line with that required for the PEA based on the revised mining plan. No environmental or social fatal flaws have been identified and Bara is not aware of any environmental or social issue that would prevent the project from proceeding to the PFS phase, during which time various potential environmental risks would need to be evaluated further.

Economic Analysis

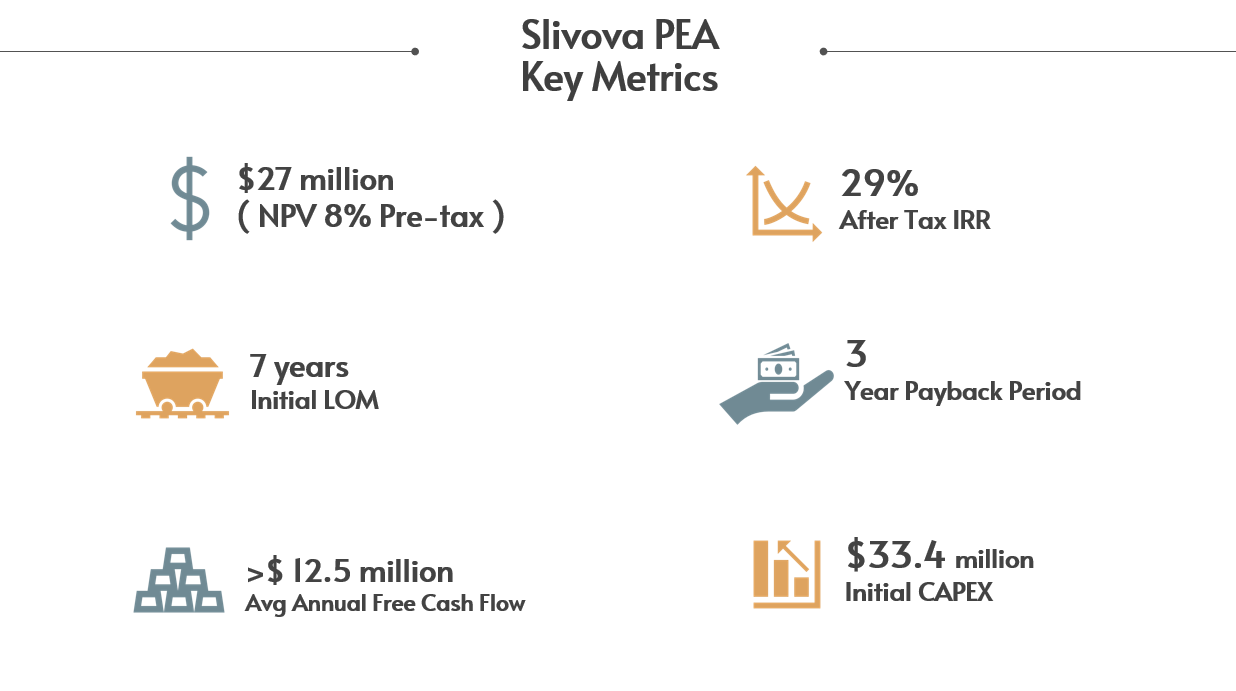

The economic analysis presented here is preliminary in nature and is based in part on Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorised as Mineral Reserves. There is therefore no certainty that the PEA presented here will be realised. PEA level economic analysis is based on the production schedule presented with capital and operating cost estimates for the Slivova Project and other information as of July 2023. The discounted cashflow analysis (“DCF”) is presented in United States Dollars (US$) in real money terms, free of escalation or inflation. Revenue has been determined through application of the recovered troy ounces produced by Slivova to the gold and silver prices as stated, less payability. Depreciation has been calculated on the assumption of that 100% of capital expenditure may be deducted from profits in the year that they are incurred (Deductibility Rate). It is assumed that all capital expenditure is eligible for deduction. A discount rate of 8% has been used for the evaluation and no tax treatment has been applied. The conceptual DCF analysis shows the Project is economic with a pre-tax net present value (“NPV”), at 8% discount rate of US$27 million, and an internal rate of return (“IRR”) of 29% with upfront capital requirements of $33.4 million, and sustaining capital requirements of $9.4 million.